how to spot a rocketship startup in AI

lessons from my job search (part 2)

Many of us optimize for the wrong things when choosing a startup to join: prestige, billion dollar valuations, or what’s trending in the news. In my last post, I shared why one should optimize for hypergrowth as well as distracting metrics to deprioritize.

But how do you identify a company experiencing hypergrowth? And how do you get intel about their metrics given the information asymmetry when looking for a job? I take a stab at answering both based on my experience interviewing at too many AI startups (46 🫣).

1. high revenue (relative to size) and steep revenue growth rate

Mirror mirror on the wall, what’s the most important metric of them all? Revenue. And revenue growth.

Revenue proves that a company has built something people need. A user parting ways with their hard-earned money is one of the best signals that they need the product, i.e. product-market fit. It also proves that the team is able to sell their product. Unfortunately, an exceptional product brings little value to the world if people don’t use it.

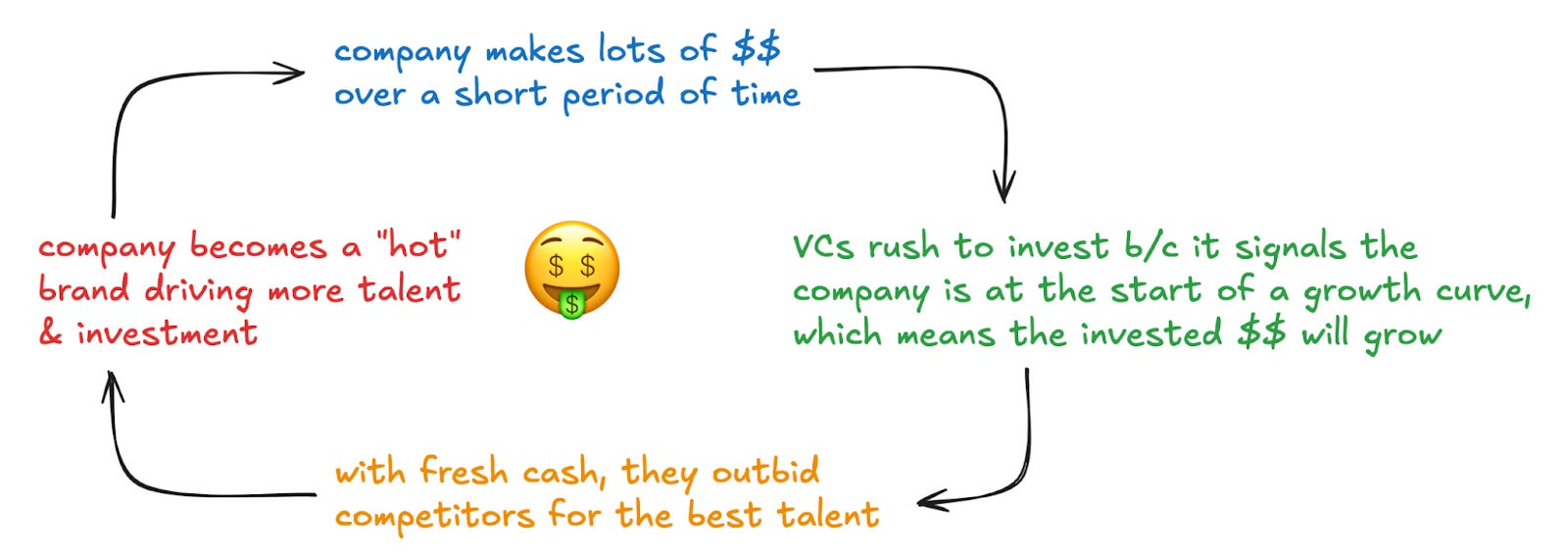

Rate of revenue growth is also key. As seen in the chart below, a steep revenue growth rate drives VC investment, talent, and brand. Even better, it creates a virtuous cycle because with money and the best people, the company is positioned to make bigger bets and generate even more revenue.

What is considered great, ok, and poor amounts of revenue?

When looking at startups as an engineer, you’re likely looking at companies of different sizes, so you can’t compare their revenue directly. These are growth rates over 6 months that are considered outstanding for SaSS companies of different sizes according to Aditya and James:

Seed: $0 → $1M ARR

Series A: $1M → $6M ARR

Series B: $5M → $25M ARR

Series C: $25M → $70M ARR

In contrast, a 3x growth rate at a small scale is considered “average”, and a 2x growth rate at a small scale is considered “poor”.

When should I ask a company about their revenue numbers?

Companies vary in their willingness to share revenue numbers with engineers, which is a signal in itself.

There are outliers with exceptional revenue like HeyGen and Harvey who will tell you how much they’re raking in in an intro call:

Most companies, however, will tell you revenue specifics once they extend an offer, which is reasonable given that it’s sensitive information.

But if you get an offer from a company and they still won’t tell you their revenue, run! Either their revenue is much lower than it should be, or they have an unreasonably secretive culture. Anecdotal evidence, but I encountered a company unwilling to share revenue specifics post offer, and their CEO abandoned the company a few months later 👀.

Even though revenue is more informative than money raised or valuation, one can’t solely look at revenue either because a company can be making money today but not tomorrow.

2. large total addressable market (TAM)

TAM represents the size of the market that the product is in. There are two main questions here:

Does the product have early traction, but a big chunk of the market yet to capture? For example, Cursor has proven v1 of their IDE in Silicon Valley with a lot of success, but software engineers globally have yet to adopt it.

Is the company working on a problem that will keep getting more important with time? For example, clean, affordable energy – one of the bottlenecks for creating general intelligence.

If both are true, hypergrowth is inevitable. It’s easier for a company to grow when the winds are in its favor: the market to capture keeps getting bigger, or there’s a large chunk of untapped potential users.

Since engineers can move freely across industries, we have the luxury of benefiting from rising tides. I.e., we can place ourselves at the right place and right time, where things outside our control are propelling growth. But it’s up to us to identify those problem spaces.

3. many loyal, obsessed customers

As an exception to “revenue growth matters above all”, there have been a handful of generational products that weren’t making much money while they were experiencing hypergrowth. What they lacked in revenue, however, they made up with exponential growth of sticky customers that they monetized later.

This is especially true of B2C companies (vs B2B) because the average person is cheap (guilty as charged). Famously, Facebook took 5 years to turn a profit, Netflix took 6, Airbnb took 9, and Uber took 151.

So what customer growth rate justifies a company not making money? Facebook got its first million users in 10 months, and then 10x’ed that to 10 million users within 2 years2. On a slightly longer timeline, Uber got to 1 million riders 2.5 years after launch, and then to 10 million 2.5 years after that3.

All this to say, a huge user base is required to compensate for low of revenue4.

What do the company’s customers really think?

For early stage companies where there’s more innate risk, I found it helpful to chat with current and churned customers. If I didn’t know any users personally, I looked on Reddit and Youtube. The goal was to get a sense of what customers love (and hate) about the product.

An added bonus is this lets you vibe-check whether the founding team is listening to their customers by seeing if the team is actively working on the pain points.

How many customers is the revenue split between?

For a traditional SaSS company, it’s better to have a lower revenue split between more customers than a higher revenue concentrated amongst a few customers. It proves that many customers have the problem, and that the team has repeatable GTM motion they can keep executing on to grow. Chunky revenue is more risky because one customer churning can lead to a big dip in revenue.

An exception to this is industries with long deal cycles. In some domains like defense whether it takes a couple years to close a deal, uneven revenue is expected and derisked because churn is less common with these hard-to-close, slow-moving industries.

4. competition: why will they win?

If a company is in a growing market (#2) and there is money to be made (#1), it likely has competitors. Competition is a good thing – it corroborates that the problem is worth solving.

But a company’s growth will eventually stall if they can’t win deals against their competition. So consider if they have a shot at building the winning product based on their current product, strategy, and team.

A strategy that helped me here was to first identify the main players. For example, in AI inference infrastructure, news sources implied it was Modal, Together, Fireworks, and OctoAI. Then, compare their revenue, deals closed, and talk to customers to determine the top two contenders. And then, interview at both. There’s only so much information you can get about a startup online, so interviewing with direct competitors gives you a better sense of how they compare. Bonus: companies are likely to give a more competitor offer if you’re choosing between them and a competitor.

the decision is not a one way door

Even though there are concrete things that indicate hypergrowth – revenue, revenue growth, market size, customer loyalty, and competitive positioning – it’s impossible to be certain of a startup’s trajectory.

Thus, it’s not irreversible if you’re wrong about a company. You leave with a lot of lessons. Similarly, you’ll likely miss opportunities that end up exploding. A mentor shared that “if you’re playing the game aggressively enough, you’ll have a list of startups that weren't obvious to you… until it was too late”, recounting how he turned down being a founding engineer at Stripe.

Ultimately, no company makes or breaks your career. The way you show up everyday shapes your career.

Special thanks to David and Aravind for shaping my thinking around this.

Thank you Mathu, Ishaan, Shanks, Abizar for reading drafts of this.

extra helpful resources

Given the power dynamics when looking for a job, it can be hard to get accurate intel about revenue, users, and competition for a company. Some other resources I found to be very helpful were:

The Information - Expensive but very high quality intel on revenue and customer growth of different companies, especially in the AI space. (I mooch off a friend - thanks Gary).

Venture Capitalists - VCs are exposed to a lot of these metrics by virtue of reading the pitch decks that come by their table. If you have genuine friends who happen to work in VC, they’ll probably give you their honest thoughts on a company you’re considering. Even if not, VCs can still be very helpful and they often respond to cold DMs. These conversations are most helpful when they’ve invested in the space you’re excited about. Best case: they invested in a direct competitor.

PitchBook - For financial reports and analysis about companies.

And even then, there are exceptions to this. For example, BeReal 70x’ed its user base over 6 months bringing it to 73 million MAU, but when the novelty of the app wore off, the user base plummeted.

how important is revenue growth if that revenue channel isn’t protected by a ‘moat’ - if important, how do you assess moat/defensibility?

There's a typo for "SaaS" in the paragraph under the revenue cycle diagram. Great points, but I too wonder whether hypergrowth is reliable. Much too often, VC-backed companies grow too fast, enshittify and then fall off just as quick. This happens less so once ARR is upwards of say 100M, but it still happens. Relevant clip: https://youtu.be/BzAdXyPYKQo?si=k5Y_bT2QLra29QUj

They have amazing revenue but unit economics is very poor, which eventually bites them back. Another issue is when they grow too fast, they may hire exponentially which causes immense slowdowns, culture wars, poor cohesion and eventually attrition. Idk really know what a good signal for growing startups is, but I think a good guiding principle is to follow really, really odd (in a good way), passionate and skilled people. Nearly always a fun place with non-linear experiences. Being in great company of cool oddballs is highly underrated imo